- Introduction

- What Exactly Is Term Insurance? (Made Simple)

- Why Term Insurance Comes Before Investing

- Term Insurance vs. Other Life Insurance Plans

- The Hidden Benefits of Term Insurance

- A Global Perspective

- Common Mistakes to Avoid

- Step-by-Step: How to Choose the Best Term Insurance Plan

- Real-Life Example: Two Families, Two Outcomes

- Final Thoughts: The Millionaire’s Secret

- FAQs on Term Insurance

Introduction

When most people talk about becoming rich, they instantly think of investments — stocks, real estate, crypto, or side hustles. I was the same. I’d chase stock tips, scroll through market updates, and dream of that one big win that would change everything.

But here’s the truth I learned: before you grow wealth, you must protect it.

That’s where term insurance steps in. People rarely get excited about it — no one brags on Instagram about paying premiums. But ask yourself: what’s the point of building wealth if it can vanish overnight? Without protection, your family could lose everything you’ve worked for. With the right plan, term insurance builds millionaire wealth by safeguarding your income, securing your loved ones, and carrying forward your dream of a richer tomorrow.

Think of it like building a skyscraper. You can have the best design and materials, but without a strong foundation, the whole structure collapses. Term insurance is that foundation.

What Exactly Is Term Insurance? (Made Simple)

Let’s cut the jargon. Term insurance is pure life insurance. You pay a small premium, and if something happens to you during the policy period, your family receives a large payout — the sum assured.

That’s it.

- No complicated investment components.

- No “returns” while you’re alive.

- Just big protection for a small cost.

For example: A healthy 30-year-old can secure $500,000 (₹4 crore) of coverage for as little as $20–$30 a month (₹1,000–₹2,000). That’s less than what many of us spend on a weekend dinner or a streaming subscription.

This is why I call it affordable term insurance — high coverage, low cost.

Why Term Insurance Comes Before Investing

One of the biggest mistakes I see people make is rushing into investments before buying term insurance.

A close friend of mine once told me proudly about his mutual fund portfolio and his plan to invest in real estate. When I asked about insurance, he laughed and said, “I’ll get it later. Not urgent.” Sadly, he faced a serious health scare two years later. By then, premiums had skyrocketed, and he could only secure limited coverage. His wealth-building plans took a massive hit.

Here’s the lesson: investments grow wealth, but without protection, that wealth can collapse overnight.

Imagine two scenarios:

- Without term insurance: A 32-year-old breadwinner suddenly passes away. The family loses income, sells investments at a loss, maybe even their home. Years of hard work gone.

- With term insurance: The same family receives a tax-free payout big enough to pay debts, cover expenses, and continue investing. The dream lives on.

That’s why I always say: protection first, growth second.

Term Insurance vs. Other Life Insurance Plans

This is where confusion creeps in. Insurance companies often push whole life, endowment, or ULIPs because they combine “insurance + investment.” Sounds great, right? Except it usually isn’t.

- Term Insurance → Low premiums, high cover, no savings element.

- Whole Life/Endowment/ULIPs → High premiums, low coverage, average returns.

Think of it this way: For the same money you’d spend on a whole life policy, you could buy a best term insurance plan with 10x the coverage and invest the rest in mutual funds or ETFs. That’s how millionaires think — keep insurance and investments separate.

Calculate your Term Insurance Premium

The Hidden Benefits of Term Insurance

People often say, “But term insurance doesn’t give me returns while I’m alive.” Here’s why that thinking misses the point:

- Low Premiums Free Up Cash for Investments

Instead of paying huge premiums on traditional policies, you save thousands and redirect it into wealth-building assets. - Peace of Mind Leads to Smarter Choices

When you know your family is protected, you stop making decisions from fear. That freedom lets you take calculated risks — like starting a business or investing long-term. - Your Wealth Journey Doesn’t End With You

Even if life takes an unexpected turn, your family continues your financial plan instead of starting from scratch.

This is why I say the benefits of term insurance go beyond numbers. It safeguards dreams.

A Global Perspective

The beauty of term insurance is that the principle remains the same everywhere: protect income at a low cost.

- US/Canada/UK: Widely used. Employer-provided insurance is common but usually not enough.

- India/Pakistan/Philippines: Term plans are very affordable, but many still buy traditional policies.

- Singapore/UAE/Nigeria/South Africa: Premiums vary, but the earlier you buy, the cheaper it is.

No matter where you are, one universal rule applies: the younger and healthier you are, the more affordable term insurance becomes.

Common Mistakes to Avoid

Even though term insurance is simple, I’ve seen people make costly mistakes:

- Underinsuring: Getting too little coverage (always aim for 10–15x your annual income).

- Waiting too long: Every year of delay means higher premiums.

- Falling for combo plans: Mixing investment with insurance dilutes both.

- Ignoring claim settlement ratios: Pick insurers with a strong record of paying claims.

This isn’t just paperwork — it’s your family’s lifeline.

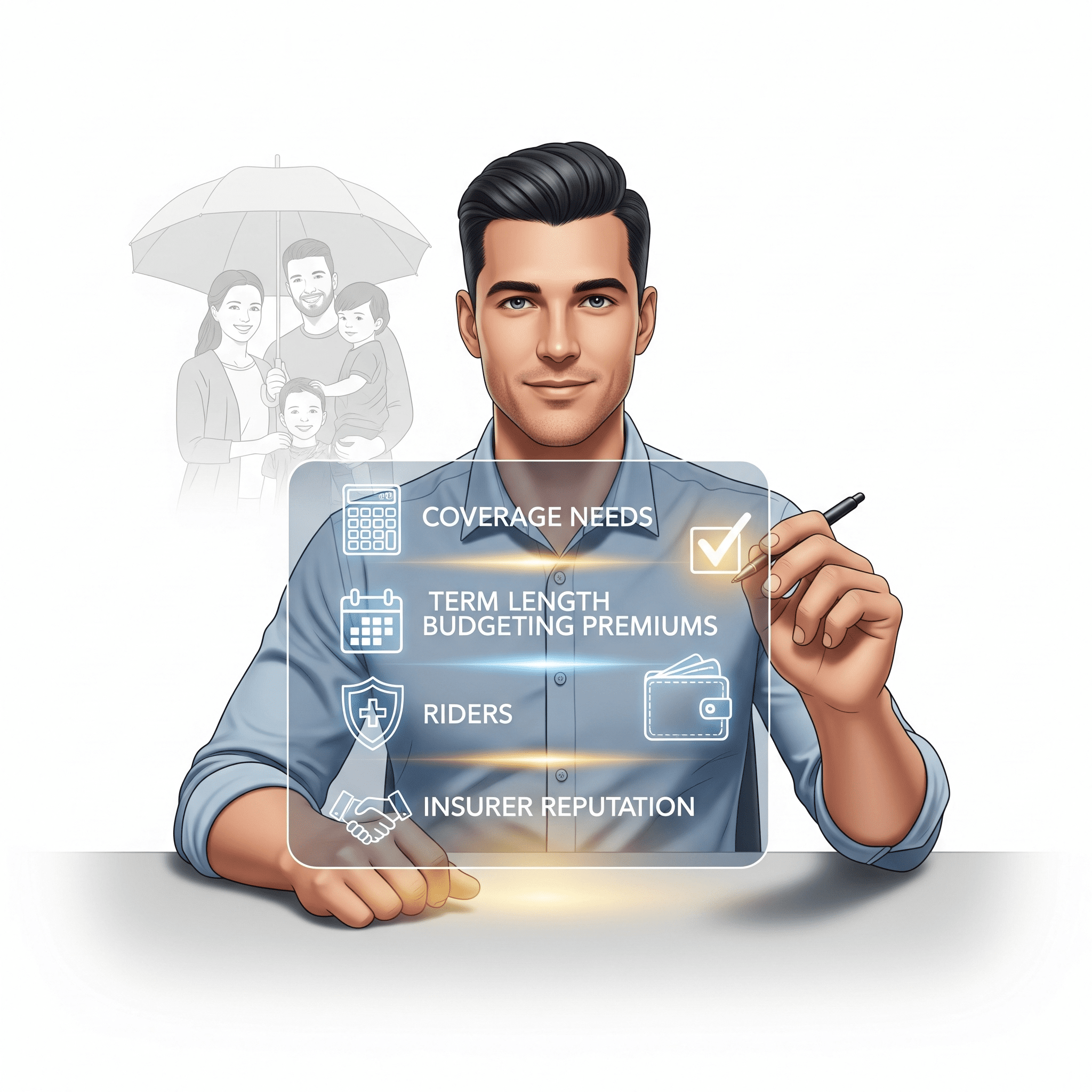

Step-by-Step: How to Choose the Best Term Insurance Plan

Here’s a process I used for myself:

- Calculate coverage needs. Add up 10–15x annual income, plus outstanding debts and future family needs (kids’ education, spouse’s retirement).

- Pick the right term. Coverage should last at least until 60–65, ideally until your major financial goals are secure.

- Set a budget. Choose a premium you can comfortably pay for decades.

- Add riders wisely. Critical illness or accidental disability riders can provide extra safety.

- Check insurer reputation. Look at claim settlement ratios and customer service.

This is how you land the best term insurance plan for your family. Simple, but powerful.

Real-Life Example: Two Families, Two Outcomes

Let me share a story.

Family A: Raj was 35, with a good job, two kids, and big dreams. He kept delaying insurance, focusing instead on investments. Tragically, he passed away in an accident. His wife had to sell their home, use up savings, and move in with relatives. Years of progress vanished.

Family B: Same age, similar background, but Raj’s colleague Arjun bought term insurance early. When he passed away suddenly, his family received a payout that cleared debts, funded his kids’ education, and gave his wife financial security. His dream of wealth didn’t die with him.

The difference? Just one decision.

Final Thoughts: The Millionaire’s Secret

Millionaires don’t buy term insurance because it’s glamorous. They buy it because they know wealth is fragile without protection.

It’s like wearing a seatbelt. You don’t expect a crash, but you wear it so you can drive with confidence. Once you’re protected, you can pursue wealth with freedom, not fear.

At richerthanyesterday.com, I believe real wealth is about progress — ensuring every tomorrow is financially stronger than yesterday. And progress begins with one unglamorous, but life-changing choice: term insurance.

FAQs on Term Insurance

Why Some People Keep Getting Richer Than You in 2025

Have you ever scrolled through Instagram or LinkedIn and thought, “Why do some people always…

Buying a Car at the Wrong Time? Avoid This Costly Mistake in 2025

The Hidden Cost of Car Ownership Buying a car feels like a big moment. It’s…

Renting vs Buying a House with EMI: Wealth Choices for 2025

A house has always meant more than just four walls — it’s a symbol of…

Best Credit Cards in 2025: The Shocking Truth Banks Don’t Want You to Know

Everywhere you turn in 2025, banks are chasing your attention with flashy ads about the…

How Term Insurance Builds Millionaire Wealth in 2025

Introduction When most people talk about becoming rich, they instantly think of investments — stocks,…

Why Skipping Health Insurance Could Ruin Your Life in 2025– Global Healthcare Costs & Protection

Introduction I’ll be honest with you—I used to think health insurance was a scam. Every…