- The Hidden Cost of Car Ownership

- The Emotional Trap Behind Buying a Car

- Why Timing Matters More Than the Car Itself

- The Real Cost of Owning a Car in 2025

- When Buying a Car Makes Sense

- Why Waiting Can Make You Richer

- Car vs Cab: Which Is Better in 2025?

- The Hidden Financial Psychology of Car Ownership

- The Smart Way to Buy a Car in 2025

- Conclusion: Buy Smart, Not Fast

The Hidden Cost of Car Ownership

Buying a car feels like a big moment. It’s exciting—like you’ve hit a new level of independence. But here’s the thing most people don’t talk about: timing matters. A lot.

In 2025, with prices climbing and financial goals harder to reach, jumping into car ownership too soon can quietly mess with your money. It’s not just the price tag. It’s the insurance, the upkeep, the fuel, the loan interest—and the fact that your cash is now tied up in something that loses value every year.

Too many people buy cars without thinking it through. They end up stretching their budget, delaying savings, and putting off bigger goals like buying a home or investing. The car might be shiny and new, but the cost? That sticks around. This isn’t about saying “don’t buy a car.” It’s about buying smart. Knowing when it makes sense, and making sure it fits into your life without throwing everything else off balance.

The Emotional Trap Behind Buying a Car

Let’s be honest—most people don’t buy a car just because they need one. It’s often about something deeper. Maybe it’s the pressure from friends, family, or even scrolling through social media and seeing everyone flaunting their new ride. That quiet voice creeps in: “Shouldn’t I have a car by now?”

Even if your current setup—public transport, ride-shares, or cabs—works just fine, it’s easy to feel like you’re falling behind. That feeling? It’s not about transportation. It’s about status. Car companies know this. In 2025, they’re masters at playing the emotional game. Flashy ads, easy EMIs, zero-down-payment deals—they make it look like owning a car is not just doable, but necessary. But just because you can afford the monthly payment doesn’t mean it’s the right move.

Understand Money Trap : Money Traps That Keep You Poor (And How to Escape Them)

Buying on impulse, driven by emotion or pressure, can lead to years of financial stress. The car might feel like a win at first, but if it’s not backed by solid planning, it can quietly drain your savings and delay bigger goals.

don’t let a shiny dashboard steer you off course. Make sure the decision is yours—not society’s.

Why Timing Matters More Than the Car Itself

Buying a car isn’t just about picking the right model—it’s about picking the right moment.

Take Alex, for example. He lands his first job and immediately signs up for a car loan. Between the EMI, insurance, fuel, and upkeep, half his salary disappears every month. By the time the loan’s paid off, the car’s worth has dropped, and he’s barely built any savings.

Now meet Sarah. Same starting point, but she holds off. She sticks to public transport and cabs for a few years, quietly saving and investing. When she finally buys her car, her investments are pulling in enough returns to cover the EMI. She gets the same dream car—but without the stress.

Both end up with the vehicle they wanted. But one paid with peace of mind, the other with financial strain. That’s the difference timing makes

The Real Cost of Owning a Car in 2025

Buying a car might feel like a smart move, but the real price goes way beyond what’s on the sticker.

The moment you drive a new car out of the showroom, it starts losing value—fast. Within five years, most cars drop to less than half of what you paid. And that’s just the beginning.

Let’s say you’re paying ₹15,000 a month on EMIs. Over five years, that’s ₹9 lakh gone—and that doesn’t even include interest. Add insurance, fuel, servicing, and random repairs, and suddenly your car is eating up a huge chunk of your monthly income.

Here’s the kicker: every rupee you spend on your car is a rupee you’re not investing. Over ten years, that missed opportunity can be massive. It could mean delaying buying a home, missing out on compounding returns, or falling short on retirement goals.

Most people don’t think about the full picture. They see the car, the comfort, the convenience—but not the long-term cost. If you’re thinking about buying, don’t just ask “Can I afford the EMI?” Ask “What am I giving up to own this car?”

When Buying a Car Makes Sense

Let’s be clear—owning a car isn’t a bad thing. In fact, for many people, it’s a game-changer. It can save time, make life easier, and sometimes, it’s just plain necessary depending on where you live or how your days look.

But the trick is buying it at the right time.

If your income has grown steadily and you can handle the EMI, fuel, insurance, and maintenance without dipping into your savings or stressing over bills, that’s a good sign. Even better if you’ve got an emergency fund tucked away—say, six months of living expenses—and you’re already investing toward bigger goals like retirement, buying a home, or your kids’ education.

A car should make your life smoother. Maybe it cuts down a long commute, helps with family errands, or gives you peace of mind when traveling late. What it shouldn’t be is a trophy or a financial strain.

If you’ve got your basics covered and the car genuinely adds value to your day-to-day, then go for it. That’s when buying a car feels less like a burden—and more like a win.

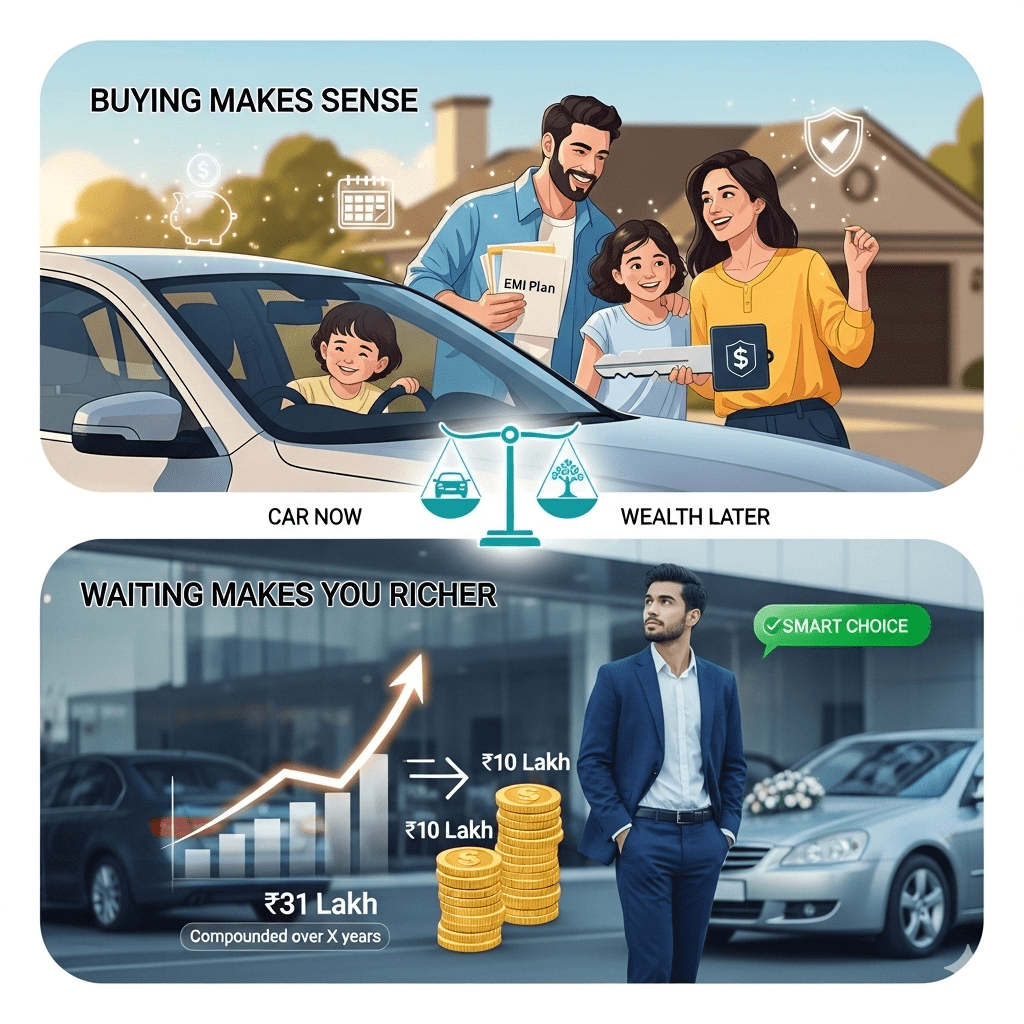

Why Waiting Can Make You Richer

Here’s something most people don’t think about when buying a car: waiting can actually make you wealthier.

Say you’ve got ₹10 lakh in hand. You could spend it on a brand-new car today—or you could invest it. If that money grows at around 12% a year, in ten years you’d be sitting on roughly ₹31 lakh. That’s not a small difference.

Now imagine holding off for a few years and picking up a well-maintained used car instead. You dodge the steep depreciation that hits new cars, and your investments keep growing in the background. You still get the car—but without the financial hit.

This is exactly why a lot of wealthy folks don’t rush into buying new cars. They let their money work for them first. When they finally buy, it’s not a stretch—it’s a reward.

It’s not about denying yourself. It’s about timing. Waiting a little can mean driving something nice and having your finances in great shape.

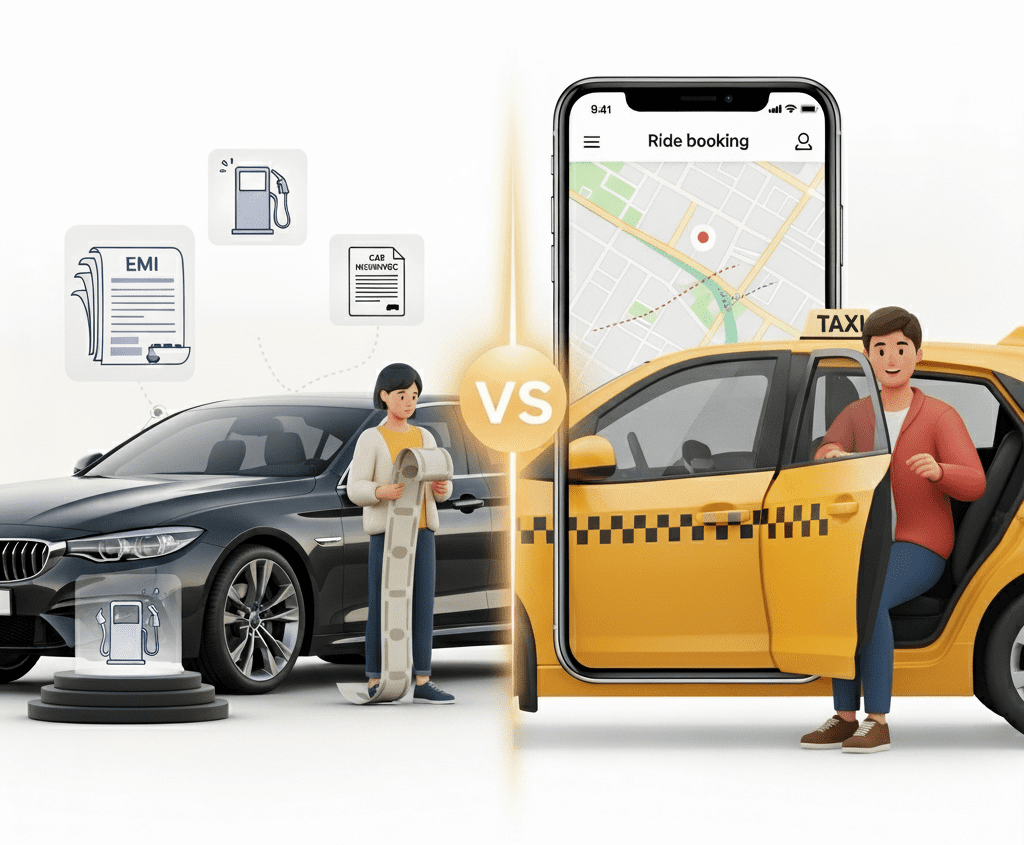

Car vs Cab: Which Is Better in 2025?

Let’s face it—owning a car isn’t the obvious choice it used to be. With Uber, Ola, Grab, and Lyft just a tap away, getting around has never been easier.

If you’re not driving more than 1,000 km a month, you might be spending less by sticking to cabs or public transport. Once you factor in fuel, insurance, repairs, and how quickly a car loses value, the math often favors ride-sharing.

But it’s not the same for everyone. If your daily travel is long, unpredictable, or you live somewhere where buses barely show up, having your own car can make life way easier. It’s not just about saving money—it’s about saving time and avoiding stress.

A lot of people assume owning a car is always the smarter move. It’s not. In cities with good public transport, cabs can be cheaper and more convenient. But in smaller towns or places with poor infrastructure, a car might be the only real option.

So don’t just follow the crowd. Look at your routine, crunch the numbers, and go with what actually fits your life.

The Hidden Financial Psychology of Car Ownership

Here’s something most people don’t realize: owning a car can mess with your head—and your wallet.

It starts small. A weekend drive here, a new gadget there, maybe a fancy upgrade just because it feels good. Before you know it, you’re spending way more than you planned. And for some, swapping cars every few years becomes a habit. It feels like progress, but financially, it’s often the opposite.

Unlike investments, cars don’t grow in value. They lose it—fast. Every upgrade, every extra expense adds up, and over time, it can quietly drain your savings.

That’s why it helps to shift your mindset. Think of your car as a tool, not a trophy. It’s there to get you from point A to point B safely and efficiently—not to prove anything or fill an emotional gap.

When you treat your car like a utility, you make smarter choices. You spend less, stress less, and keep your financial goals on track.

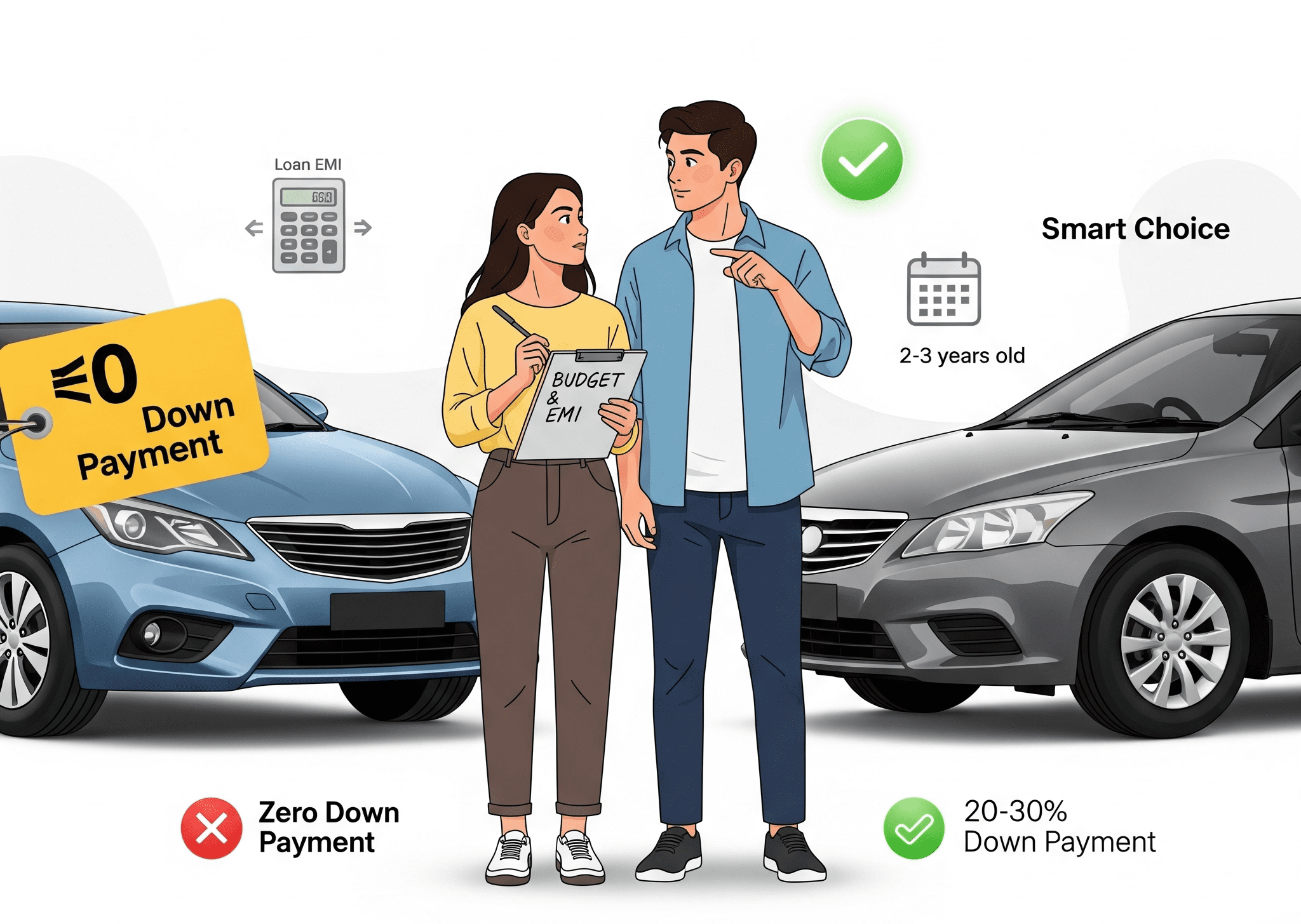

The Smart Way to Buy a Car in 2025

If you’ve decided it’s time to buy a car, great—but don’t rush into it. A few smart moves can save you a ton of money and future headaches.

First off, consider buying a car that’s 2–3 years old. You’ll skip the steepest part of depreciation and still get something that feels almost new. It’s one of the easiest ways to get more value for your money.

Also, steer clear of those tempting zero-down-payment deals. They might look easy upfront, but they usually come with higher interest and longer repayment periods. If you can, put down at least 20–30%—it’ll lower your loan burden and keep things manageable.

When it comes to EMIs, try to keep them within 10–15% of your monthly income. That way, you’re not stretching your budget or sacrificing other financial goals. And think long-term: if you can hold onto the car for 7–10 years, you’ll get the most out of your investment and avoid the trap of frequent upgrades.

Bottom line—buying a car doesn’t have to derail your finances. With a little planning, you can enjoy the ride and stay on track with your bigger goals.

Conclusion: Buy Smart, Not Fast

In 2025, the real trap isn’t buying a car—it’s buying one too soon. Jumping into ownership before your finances are solid can turn a dream into a drain. But if you wait, plan, and let your money grow first, that same car can feel like a reward instead of a regret.

Before you sign that EMI form or chase the newest model, take a moment. Ask yourself: Do I actually need this right now—or am I just feeling the pressure to keep up? That one question could save you lakhs. It could even set you up for a stronger, wealthier future. Because in the end, real success isn’t about what’s parked in your driveway—it’s about having the freedom to make choices without stress. So take your time. Make it count.

Why Some People Keep Getting Richer Than You in 2025

Have you ever scrolled through Instagram or LinkedIn and thought, “Why do some people always…

Buying a Car at the Wrong Time? Avoid This Costly Mistake in 2025

The Hidden Cost of Car Ownership Buying a car feels like a big moment. It’s…

Renting vs Buying a House with EMI: Wealth Choices for 2025

A house has always meant more than just four walls — it’s a symbol of…

Best Credit Cards in 2025: The Shocking Truth Banks Don’t Want You to Know

Everywhere you turn in 2025, banks are chasing your attention with flashy ads about the…

How Term Insurance Builds Millionaire Wealth in 2025

Introduction When most people talk about becoming rich, they instantly think of investments — stocks,…

Why Skipping Health Insurance Could Ruin Your Life in 2025– Global Healthcare Costs & Protection

Introduction I’ll be honest with you—I used to think health insurance was a scam. Every…