- The Early Struggle – When Small Spends Become Big Problems

- Learning to Prioritize – Needs vs. Wants

- The Power of Saying No – And Feeling Good About It

- Discovering Local Hacks – Bhubaneswar’s Budget-Friendly Secrets

- The Emotional Side of Money – Guilt, Pride, and Self-Control

- Building Long-Term Habits – From Tracking to Thriving

- Conclusion – A New Relationship with Money

The 50-30-20 rule was the game-changer I didn’t know I needed when I first moved to Bhubaneswar. I wasn’t just dragging a suitcase—I was carrying excitement, nerves, and that gut feeling that something was about to shift. Everyone had hyped the city as peaceful, green, and soulful. And honestly? They weren’t wrong. The auto rides, roadside chai, and crisp temple mornings felt grounding and magical.

But no one warned me how quietly money slips away if you’re not watching. I wasn’t chasing luxuries—no designer bags, no fancy dinners. Most of my savings went into ordinary things: setting up a corner of my room, buying groceries that I thought would last but never did, and slowly syncing myself with Bhubaneswar’s pace. Yet, somehow, the numbers never added up. My budget looked perfect on paper, but my bank account told me a different story. Honestly, it felt like my wallet was on a diet I hadn’t agreed to.

That’s when I realized that separating needs from wants wasn’t optional—it was survival. The 50-30-20 rule didn’t just guide my spending, it gave me back control.

The Early Struggle – When Small Spends Become Big Problems

The problem wasn’t one big purchase. It was the small, everyday things — the ones that don’t seem like a big deal at the time. An auto ride here, a takeaway coffee there, ordering dinner because I was too tired to cook, buying that one kurti just because it was on sale. The danger of these tiny spends is that they don’t feel like “real expenses” until they pile up. And oh, they do pile up.

I remember one particular week. I had told myself I’d spend very little. But then one evening I was tired and ordered a ₹250 meal online. The next day, my friend called me for a quick coffee — another ₹150 gone. Then there was an auto ride because it was raining — ₹120. By the weekend, a spontaneous visit to a clothing store added ₹600 to the list. None of these were “big” purchases. But by the end of the week, I had spent more than ₹1,500 without even realizing it. That was the moment I understood — it’s the invisible leaks that sink the ship.

Learning to Prioritize – Needs vs. Wants

Getting real with myself wasn’t instant. I began jotting down every single expense—no matter how tiny. At first, it was just curiosity. But two weeks in, the truth stared back: a huge chunk of my money was going toward pure wants. Not bad in itself—life’s meant to be enjoyed—but I was saying “yes” to every impulse without pausing.

So I made a rule: Before I spend, I ask, “Is this a need or just a want?” Simple, but game-changing. Sure, I’d still say yes sometimes—because denying yourself a cold coffee on a blazing day feels criminal—but more often, I’d pause and put things back.

It wasn’t about cutting joy.

For me, it slowly became less about strict numbers and more about spending with intention. First, I made sure the non-negotiables were covered—rent, groceries, basic bills. Once those were out of the way, I gave myself permission to enjoy the little extras if the budget still had breathing space. That way, I didn’t feel guilty about ordering food on a Friday night or catching a movie. Over time, that tiny shift helped me save without feeling restricted, and I found myself naturally leaning into the 50-30-20 rule. Not perfect, but progress.

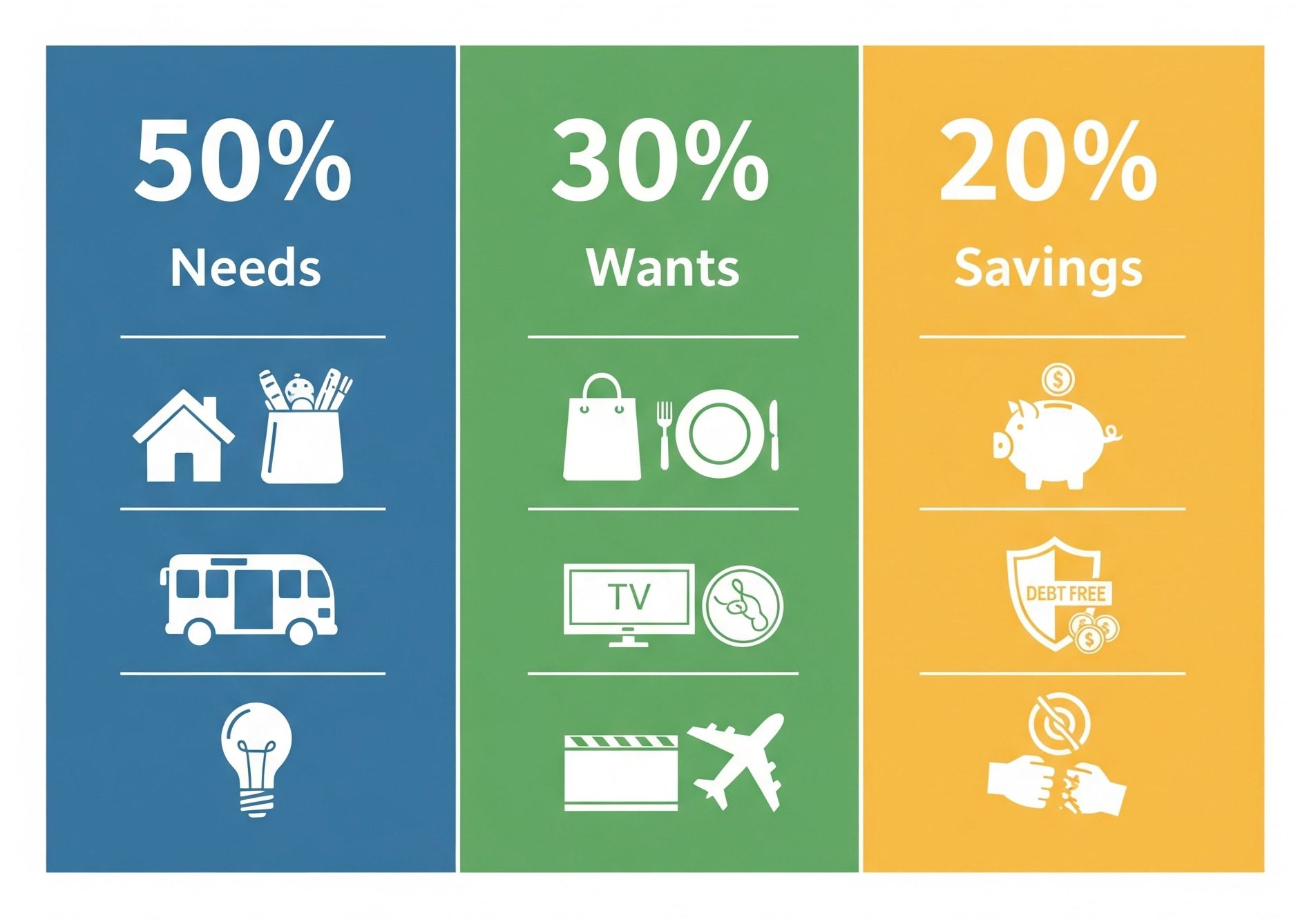

Here’s the 50-30-20 rule in finance explained in 3 simple pointers:

-

50% Needs – Half of your income goes to essentials like rent, groceries, transport, and utility bills.

-

30% Wants – Use 30% for lifestyle choices such as shopping, dining out, streaming subscriptions, or travel.

-

20% Savings – The remaining income should strengthen your savings account, build an emergency fund, or repay debt.

Calculate your budget with 50-30-20 rule Calculator

The Power of Saying No – And Feeling Good About It

Honestly, one of the hardest things for me was learning that saying “no” doesn’t make you cheap or boring. In the beginning, I used to feel awful when I skipped outings or said no to plans. A part of me worried people would think I was being distant. But over time, I realised the people who actually care about you don’t measure friendship by how much you spend.

So I started making small swaps. If friends wanted to catch up, I’d say, “Come over, I’ll make chai and pakoras,” instead of another café bill. For short trips, I’d walk or share an auto instead of booking one solo. Funny thing is, most of my friends didn’t mind — some even preferred it. It felt less about the money and more about the time together.

Every “no” I said — whether to a random online order or another late-night food delivery — gave me a little sense of control. It wasn’t just about saving a few hundred rupees. It was about making choices on my own terms. Slowly, that helped me follow the 50-30-20 rule without feeling like I was punishing myself.

Discovering Local Hacks – Bhubaneswar’s Budget-Friendly Secrets

One of the unexpected joys of Bhubaneswar is that you don’t have to spend a fortune to enjoy life here. Once I started looking, I found little hacks everywhere. Fresh vegetables from local markets were cheaper and fresher than supermarket ones. Street food — from piping hot chai to crispy pakoras — was not only budget-friendly but also gave me that feeling of being part of the city’s rhythm.

I also learned that walking or cycling not only saved money but also gave me a deeper connection with the place. I discovered tiny bookshops, quiet temples, and hidden cafés that I would’ve missed if I’d just zipped around in autos. And the best part? I wasn’t spending much at all.

The Emotional Side of Money – Guilt, Pride, and Self-Control

Money isn’t just about numbers on a bank screen—it’s emotional. I realised that a lot of my spending had nothing to do with actual needs. Half the time, it was stress, boredom, or just wanting a quick mood boost. That late-night coffee run? Honestly, it wasn’t about caffeine. It was just me looking for a break from work. That random online dress? More about the dopamine rush than the dress itself.

What changed things for me was separating emotions from expenses. Now, whenever I feel the itch to spend, I pause. Sometimes I take a short walk, call a friend, or even put on an old comfort movie instead. Do I succeed every single time? Nope. But even skipping one impulse buy makes me feel proud. It’s not just saving ₹200—it’s proof I can actually stick to my plan.

The 50-30-20 rule gave me a framework for this. It reminded me that wants are fine—as long as they don’t hijack the whole budget. That balance is where I finally found control.

Building Long-Term Habits – From Tracking to Thriving

What began as tiny tweaks slowly turned into habits. I started tracking where my money went—not with fancy apps or spreadsheets, just a plain notebook. Every weekend, I’d total it up. Some weeks were smooth, others messy, but just the act of checking kept me grounded in my budget.

I also set small savings goals. Nothing dramatic—just ₹500 a week. But that consistency worked. Over time, I saw a little buffer in my account. That cushion? It was new. It felt like breathing space.

The best part? I didn’t feel restricted. I still hung out with friends, still sipped my coffee, still picked up the occasional kurti. But now, those wants felt intentional. I wasn’t spending out of habit—I was choosing joy, not chasing it. That’s when the 50-30-20 rule stopped being theory and started feeling like freedom.

Conclusion – A New Relationship with Money

Moving to Bhubaneswar didn’t just mean learning new roads and new routines—it completely changed the way I looked at money. I stopped treating it like a list of restrictions and started treating it like a tool. Now, I spend with more awareness, I plan instead of panic, and I know it’s okay to enjoy small pleasures as long as I stay in control of my bigger goals. That balance between saving and living? That’s what makes money feel less stressful and more freeing.

Now, when I check my account at month’s end, I don’t feel that sinking “Where did it all go?” panic. I feel calm. I know where my money went, why I spent it, and what I’ve saved. That sense of control? It’s worth more than any impulse buy. And if you’re looking to build that same peace of mind, I share everything I’ve learned—mistakes, mindset shifts, and practical tips—on richerthanyesterday.com. Because financial freedom isn’t about perfection. It’s about progress.

Why Some People Keep Getting Richer Than You in 2025

Have you ever scrolled through Instagram or LinkedIn and thought, “Why do some people always…

Buying a Car at the Wrong Time? Avoid This Costly Mistake in 2025

The Hidden Cost of Car Ownership Buying a car feels like a big moment. It’s…

Renting vs Buying a House with EMI: Wealth Choices for 2025

A house has always meant more than just four walls — it’s a symbol of…

Best Credit Cards in 2025: The Shocking Truth Banks Don’t Want You to Know

Everywhere you turn in 2025, banks are chasing your attention with flashy ads about the…

How Term Insurance Builds Millionaire Wealth in 2025

Introduction When most people talk about becoming rich, they instantly think of investments — stocks,…

Why Skipping Health Insurance Could Ruin Your Life in 2025– Global Healthcare Costs & Protection

Introduction I’ll be honest with you—I used to think health insurance was a scam. Every…